Executive Briefing|January 13, 2022

Health Plan Success Drivers in 2022 (A Renewed Focus on Performance and Execution)

Share:

Health Plan Success Drivers in 2022 (A Renewed Focus on Performance and Execution)

Every January, we provide our perspective on areas of increasing importance and value for health plans for the upcoming year. Our prospective view of 2021 focused on the need for health plans to strike a balance between innovation and investment in evolving markets with the management of the challenges (and opportunities) of the COVID-19 pandemic. Our 2021 predictions – focused on growth in government programs, strengthening of value-based care (VBC) programs, acceleration of multi-modal consumer engagement models, and preparation for vaccine distribution – fared well in light of rapidly shifting conditions.

As we look towards 2022, our focus has shifted from prediction of new areas of importance and value to an emphasis on what is needed from health plan performance to realize success in the coming year. Specifically, success in 2022 (and beyond) will depend on the execution of strategies that may have been developed and defined in prior years.

→

For 2022, we are particularly focused on:

1. Evaluating and Reacting to Program Successes and Failures (To Prove the ROI)

2. Succeeding in Medicare Advantage (Beyond Table Stakes Capabilities)

3. Making Value-Based Care Mainstream (But Only if it Evolves)

4. Achieving Administrative Scale (Without Growing)

5. Meeting the Demands of the COVID Consumer (Who Has New Expectations of Engagement)

Evaluating and Reacting to Program Successes & Failures (To Prove the ROI)

Plans that apply rigor and discipline from development through evaluation and governance of its programs are more favorably positioned to achieve desired outcomes. In particular, medical cost containment measures—intended to influence both unit cost and utilization—are more important than ever for plans to remain viable. This especially rings true given the uncertainties and competitiveness of today’s managed care environment. A health plan’s ability to deliver cost savings for itself and its customers often hinges on the success of these medical cost containment programs, which are typically designed around a variety of focused clinical areas (e.g., behavioral health, orthopedics, pharmacy).

The need for this discipline is not limited to medical cost management. Across numerous business functions, a plan must take a more rigorous examination of its programs and vendors to determine whether there is a return on investment. This discipline should be applied broadly across the health plan including the effectiveness of sales channels, the value of supplemental benefits and the efficacy of member engagement programs.

While these programs are critical for improved clinical outcomes and financial performance, most plans struggle to quantify or articulate the concrete value of their existing program portfolio. Like any professional investment fund, plans should think and operate like active managers of their cost management and quality improvement program portfolio. As any successful portfolio manager knows, program performance should be measurable, monitored, and influential in near- and long-term decision making.

The Issue:

Oftentimes, plans have either not established processes to consistently measure program effectiveness or do not have access to the necessary data to evaluate program success. Both of these scenarios often lead to continued program proliferation without a basis in evidence. Even when plans can measure program performance, internal factors swaying judgment of success vs. failure can present another major challenge. Plans risk investment decisions being based on personal vendor relationships, internal biases, or other factors unrelated to the corresponding value delivered by each program.

Separately, plans also face the challenge of clearly and accurately attributing improved outcomes to specific programs or combinations of programs, particularly as polychronic members may be enrolled in and benefitting from multiple programs. For example, an obese patient with diabetes may: a.) participate in a plan’s disease management program, b.) have access to condition management tools offered by the health plan (e.g., remote monitoring devices, nutritional guidance), and c.) be enrolled in a value-based payment program. In this example, it would be difficult for a plan to isolate and evaluate the discrete (and exclusive) impact of each program on the member’s outcomes.

What Plans Should Do:

1. Consider Measurement and Framing in Program Design:

During the program design phase and prior to launch, plans should align on program objectives, evaluation criteria and methodology (including KPIs and metrics), and critical success factors. A single metric to measure program value may not be the most useful depending on program design, population participation, and other factors, so plans should consider a mosaic approach to value measurement that synthesizes multiple metrics to build a comprehensive story of value creation. Additionally, the definition and design of value measures can establish data collection and other technical requirements upfront to ensure that value measurement can be sustained throughout the program lifecycle.

2. Stay Grounded in Methodology, Measurement Criteria, & Impact of Member Duration:

It is imperative for plans to cultivate a culture of objectivity, striving for the academic and data-driven truth unencumbered by internal politics or program ownership. Firstly, plans must establish measurement frameworks to monitor program performance on a timebound or periodic basis. Plans that stay rooted in the original program objectives and their corresponding established measures will remain well-positioned. Additionally, plans must also ensure that program evaluation frameworks consider the full duration of program returns for participating members. For example, MA members have longer enrollment durations and therefore, returns on health and wellness programs and investments (e.g., fitness, nutrition, remote monitoring technology) span multiple years. By contrast, ACA enrollees have greater churn, decreasing likelihood for returns through longer-term investments. As plans develop methodology frameworks, it is critical to identify cohorts for measurement (e.g., risk vs. ASO, VBC vs. non-VBC) and contemplate outcomes beyond cost of care, including clinical quality outcomes, member experience, and operational measures.

HealthScape’s three-year study (2017-2019) of Highmark Inc.’s group customers found that integrated medical and pharmacy benefits lowered costs, improved health outcomes and strengthened member engagement.

3. Develop Sustainable Reaction Plan with Appropriate Governance:

Upon program launch, plans must embrace agility with reaction plans to optimize program performance. Plans should consider multiple sources and years of data in the evaluation of program success and commit to instituting program changes based on results. Such changes may translate to fixing program design issues, augmenting the existing program or sunsetting a plateauing program. A culture that celebrates and learns from failure (i.e., “failing fast”) will be poised to pivot quickly and implement changes that enable longer-term success. As such, programs that fail to deliver on intended objectives should be disbanded to reallocate internal resources and investments. Like any good portfolio manager, plans should “divest assets” not generating the intended returns to re-deploy capital and seek additional returns. Ultimately, plan leadership should remain nimble in ensuring that the results of program evaluations and governance drive decision-making, process re-engineering, investment decisions and other programmatic changes.

Succeeding in Medicare Advantage (Beyond Table Stakes Capabilities)

With 26M seniors currently enrolled, Medicare Advantage (MA) has long been a strategic focus for plans hoping to capitalize on growing senior demographics. This focus will only sharpen in the coming years as the share of all Medicare beneficiaries enrolled in MA is expected to increase to 51% by 2030. Despite the market opportunity, success in MA is challenging as it requires unique “table stakes” capabilities, including differentiated product development, efficient cost management, a competitive provider network, active cost management strategies, achievement of 4+ Star Ratings, and accurate and compliant coding capture for risk adjustment.

The Issue:

In addition to focusing on the numerous “table stakes” capabilities listed above, MA plans face a host of challenges:

1. Increasing competition and challenges to differentiate

In 2021 the average senior could select from 33 plans, leading to market crowding and consumer confusion. As zero-dollar premium plans become the norm, products become richer and supplemental benefits proliferate, making it harder for plans to differentiate.

2. Lack of diversification in the MA portfolio

Given the competitive environment described above, plans must look to other opportunities to grow and differentiate outside of traditional individual MA-PD.

3. Distribution channels have become more costly

MA plans are using an increasing number of distribution channels to remain competitive, meet consumers’ preferences towards digital, and respond to the COVID-19 crisis. Plans must understand the characteristics and performance of individual distribution channels – each of which attract different consumer profiles with varying acquisition costs – to actively manage and optimize their channel mix.

4. Increasing levels of turnover

While MA members have historically been “sticky,” these new distribution channels and the ultra-competitive environment are creating more opportunities for customers to shop and switch, resulting in turnover that makes it difficult for MA plans to realize a return on investment in risk adjustment and care management strategies.

What Plans Should Do:

Optimize Distribution Channel and Retention Performance:

MA plans should evaluate distribution channel performance across geographic markets, informing capabilities that optimize sales, retention, and business performance. Evaluations should include:

- Benchmarking financial and operational performance metrics as well as demographic trends for channels

- Conducting channel optimization and scenario planning to test channels, geographies, and continuous factors aligning to performance metrics; running scenario modeling to rebalance distribution mix based on maximized sales volume and member lifetime value

- Assessing changes to partnerships and operations to improve channels’ performance, focusing on retention (e.g., life of lead studies, welcome and on-boarding practices)

Assess Product Portfolio Expansion Opportunities:

MA plans must ensure that they understand the market opportunity, competitive landscape, and critical success factors for the non-individual products, notably:

- Special Needs Plans (SNP): Confirm adherence to regulatory requirements (e.g., Model of Care) along with capabilities unique to the population (e.g., elevated clinical management programs / clinical teams, member education and engagement, curated provider networks)

- Employer Group Waiver Plans (EGWP): For plans with a strong commercial presence, focus on employers that offer retiree coverage with emphasis on the value proposition of MA vs. wrap / supplemental products. Success in EGWP markets is predicated on EGWP-specific operating and actuarial procedures, an aligned commercial and Medicare sales process inclusive of coordinated employer communication and clinical and risk adjustment programs that reflect unique geographic and network considerations

Evaluate and Optimize Supplemental Benefits:

To succeed in the supplemental benefit arms race, plans must reframe their view of supplemental benefits. Historically, there has been a singular focus on supplemental benefits as a marketing tool; future definitions must expand beyond this to account for the meaningful impact that these benefits can have on enrollment, clinical outcomes and medical cost. According to a joint study conducted by HealthScape, Pareto Intelligence and Consumer Healthcare Products Association (CHPA), only 20-35% of members utilize the over-the-counter (OTC) benefit at least once a year, revealing a significant untapped opportunity. A successful supplemental benefits strategy includes:

- Analysis and understanding of the impact that supplemental benefit options have on member enrollment, member engagement, clinical outcomes, medical cost reduction and member satisfaction

- Integration of results from analysis into broader health plan strategy efforts around care management, outreach and customer service / in-bound calls

Making Value-Based Care Mainstream (But Only if it Evolves)

Over the past decade, value-based care has become so entrenched in healthcare discourse that many would argue that it is now a normative part of health plan strategy and business model formulation. Companies with private equity and venture investment backing have pushed value-based economic models as core to their business, while new mega entrants such as Walmart Health continue to expand their clinical-care footprint through improved accessibility, choice, clinical quality and cost savings. In light of increasing state and federal regulatory efforts related to value-based reporting (and requiring a shift to these payment methodologies), health plans and provider systems alike are more consistently quoting the percent of payments / revenue tied to value-based payments.

The Issue:

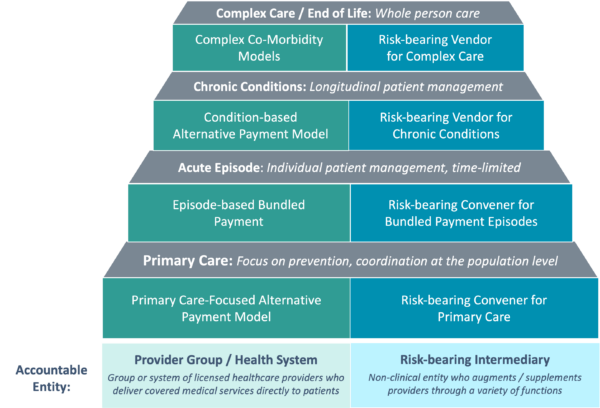

Despite these overarching trends, the actual impact that value-based payment has had on many health plans’ economic and clinical models has been limited with general plateaus in both savings and aligned / attributed individuals. Stagnating progress has led many to question the merits of accelerating primary care-focused models and has shifted focus on advancing the next generation of VBC which is increasingly inclusive of specialist-based models and incentives for alternative care sites (e.g., retail, home, and virtual). Our recent publication dives deeply into the opportunities of building specialty-based value programs (see Figure 1).

What Plans Should Do:

1. Objectively Evaluate Existing Programs:

Many plans have a menu of value-based investments (e.g., primary care-based Accountable Care Organizations [ACOs], patient-centered medical homes [PCMHs]); it is time to assess the true impact of these programs on care delivery transformation, quality and cost outcomes. Part of this assessment includes determining the time horizon required for programs to yield the benefits that offset financial and resource investments. ROI estimations on these programs should lead to defining areas of the programs that need to change.

2. Identify “Carve Out” Populations:

Health plans should identify populations, if any, that have either been: a.) excluded from certain programs due to limitations of attribution methodologies or b.) have been under-managed as a result of predominant spending and care needs residing in the specialist care environment.

3. Confirm Operational Readiness for Risk Arrangements:

Health plans need to confirm readiness of their technology, platform(s) and other operational capabilities to support risk arrangements with providers, and conversely, how those capabilities will interface with the provider assuming risk. Oftentimes, plan capabilities and supporting infrastructure lack the sophistication to realize value-based care deals despite provider (both primary and specialty care) interest.

4. Develop Specialty-Based Care and Payment Models:

Determine opportunities to either carve out select members from primary care models (to avoid duplication across multiple programs) or create models which are “paid” for by the primary care programs. These models could be procedure-based (e.g., orthopedic bundles) or condition-based (e.g., management of members with congestive heart failure). One advantage of these carve-out programs is that given their focus, they are relatively quick to develop and deploy – often within 6 months – allowing the opportunity to quickly assess financial impact.

5. Continue to Invest in Primary Care / Specialty Care Coordination:

Given the increased complexity from the advent of specialty programs, plans that develop more robust reporting and improve communication with providers and across primary care and specialty providers in value-based models are most likely to realize their investments.

Figure 1: Portfolio Framework for Speciality Model Identification

Achieving Administrative Scale (Without Growing)

As the overall growth of the insured population has leveled, plans concentrated in specific geographies (e.g., single-state BCBS plans, regional and community health plans) have struggled to identify growth opportunities. These midsize and smaller plans cannot realize the administrative cost efficiencies of the Nationals or larger health plans and their lack of scale continues to negatively impact their competitive positioning. The combination of widening labor costs, an influx of differentiated technology platforms, and fixed security costs leave them more vulnerable to competition than ever.

The Issue:

The endless challenge of managing administrative expenses (often exceeding 12-14% or even higher in certain lines of business [LOBs] with sub-scale plans) has become more pronounced for smaller plans in the past several years as growth and diversification opportunities are largely concentrated with the Nationals. Plans with high administrative expense ratios are more susceptible to swings in medical cost and other adverse events, making the ability to manage such changes paramount to sustainable profitability. Many smaller plans have not looked under the hood of their underlying administrative cost structure and instead have focused on other internal strategies, creating an opportunity to reexamine this area.

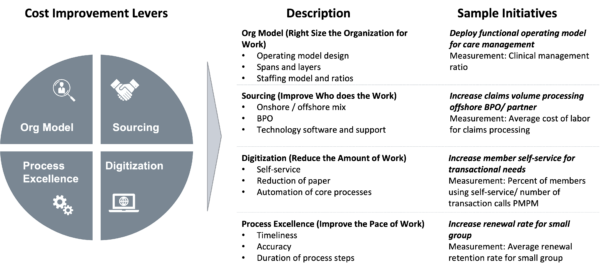

Figure 2: Applying Consistent Levers for Success

What Plans Should Do:

1. Analyze Comprehensive Cost Infrastructure:

Plans should conduct a judicious review of their entire internal cost structures, quantify and bifurcate their impact by LOB and apply a consistent set of cost improvement levers to identify the full potential efficiency opportunity (see Figure 2).

2. Understand Impact of Multiple LOBs / Diversified Plays:

Product diversification can strain organizations if expansion strategies are not well-coordinated or proactively managed. Plans should assess the impact of each line of business on margin to inform a well-balanced product portfolio.

3. Institute a Formalized Operational Review Process:

Taking stock from the disciplined Nationals, plan leaders should develop and deploy a monthly operational review process to evaluate operational target metrics against performance. Plans that apply the principles of lean management, focus on process automation, prioritize metric-based cost improvements and rationalize strategic partnerships to drive a lower administrative footprint will exert increasing competitive influence over the larger plans.

4. Invest in Differentiated Capabilities:

Smaller or regional plans will always be financially and operationally stretched to compete at scale which is why a local and community-based focus augmented by deeper member connections and provider relationships enable a competitive advantage. As plans look to streamline operations to ensure a competitive cost structure, they will need to identify opportunities to reinvest savings into capabilities that create market advantages.

Meeting the Demands of the COVID Consumer (Who Has New Expectations of Engagement)

It is likely no surprise that the COVID-19 pandemic has greatly impacted consumer preferences and behavior. While it is too early to tell which practices from “this new normal” will become permanent, we anticipate that the combination of evolved consumer behaviors and a continued push from the industry and regulators will impact health plan’ approach to the consumer experience. The pandemic has shifted consumer attitudes as they increasingly value a holistic approach to health (i.e., integration of behavioral and physical health), have a greater affinity to digital experiences and are more open to site of care shifts. Additionally, regulators are accelerating consumer-driven initiatives as evidenced by the push towards price transparency and increasing emphasis on member survey results in Star rating calculations. Serving the needs of consumers while staying abreast of regulatory policies presents plans with opportunities and challenges to meaningfully engage consumers.

The Issue:

A fundamental tenet of healthcare is to put members first; too often, care delivery and coverage have taken a one-size-fits-all approach. Plans have been slow to adopt personalized and digitized approaches to member engagement, stemming from a lack of sophisticated understanding of the consumer as well as outdated and manual analytics functions. Historically, investments in consumer experience have been expensive and their return has not always been clear. As consumer preferences evolve, the old school, pre-pandemic models will no longer move the needle in critical capabilities for member acquisition, care management, customer service and member retention. Furthermore, consumer engagement challenges are exacerbated by new entrants and well-funded health technology companies that bring a fresh approach to health engagement.

What Plans Should Do:

1. Develop Consumer-Centric / Member Engagement Solutions:

To compete with offerings from Accolade, Quantum Health and other Nationals that have grown in popularity in the past five years, plans need a unique consumer advocacy approach and engagement model. Effective member engagement, which we detail in this Executive Brief, relies on data-driven insights and plans that deploy consumer-centered solutions to support transparency and navigation.

2. Bridge the Gap Between Virtual and Physical Care:

As consumers demand digital and virtual care, plans have an opportunity (and obligation) to ensure they do not let virtual and digital care become disconnected fragments of healthcare. Plans can better satisfy consumer expectations and drive longer term success through reimbursement and coordinated strategies between physical and virtual care.

3. Invest in an Integrated Behavioral Health Approach:

The pandemic highlighted the vulnerabilities of the existing behavioral health care delivery system as well as the disconnect between physical and behavioral health management. Plans should reinforce the importance of a personalized, whole-person engagement model through investments in coordinated care programs, integrated technology platforms, and predictive analytics that connect data from behavioral, medical, pharmacy and social assets. We delve into specific strategies for plans to evolve from traditional models to the next generation of behavioral health solutions in this Executive Brief.

4. Tailor Benefit and Product Design to Local Appetites:

While many plans continue to chase the latest and greatest supplemental benefits, local and community-based plans should think about levers that differentiate their communities and develop programs that reinforce the local value proposition (versus always competing on the latest supplemental benefit option). For example, Emory Healthcare and Kaiser Permanente launched a new care model in 2018 that provides Kaiser Permanente members with a fully integrated healthcare experience exclusive to Emory in the Atlanta metro area.

5. Elevate Member Experience with Virtual / Digital / Home First Products:

Within a truncated time period, COVID-19 rapidly accelerated the use of virtual health and digital first products particularly within younger, healthier cohorts which we detail in this Executive Brief. Consumer appetite for these products is met through consumer-directed, virtual care solutions that serve as a one-stop shop for delivery of efficient care with greater engagement.

HealthScape Can Help

The healthcare ecosystem is amidst a fundamental shift with a renewed focus on performance. Success in 2022 will be marked by execution of strategies that many health plans likely developed in prior years. With a focus on long-term progress, our team has partnered with healthcare organizations to transform ongoing uncertainty into sustainable strategies and programs.